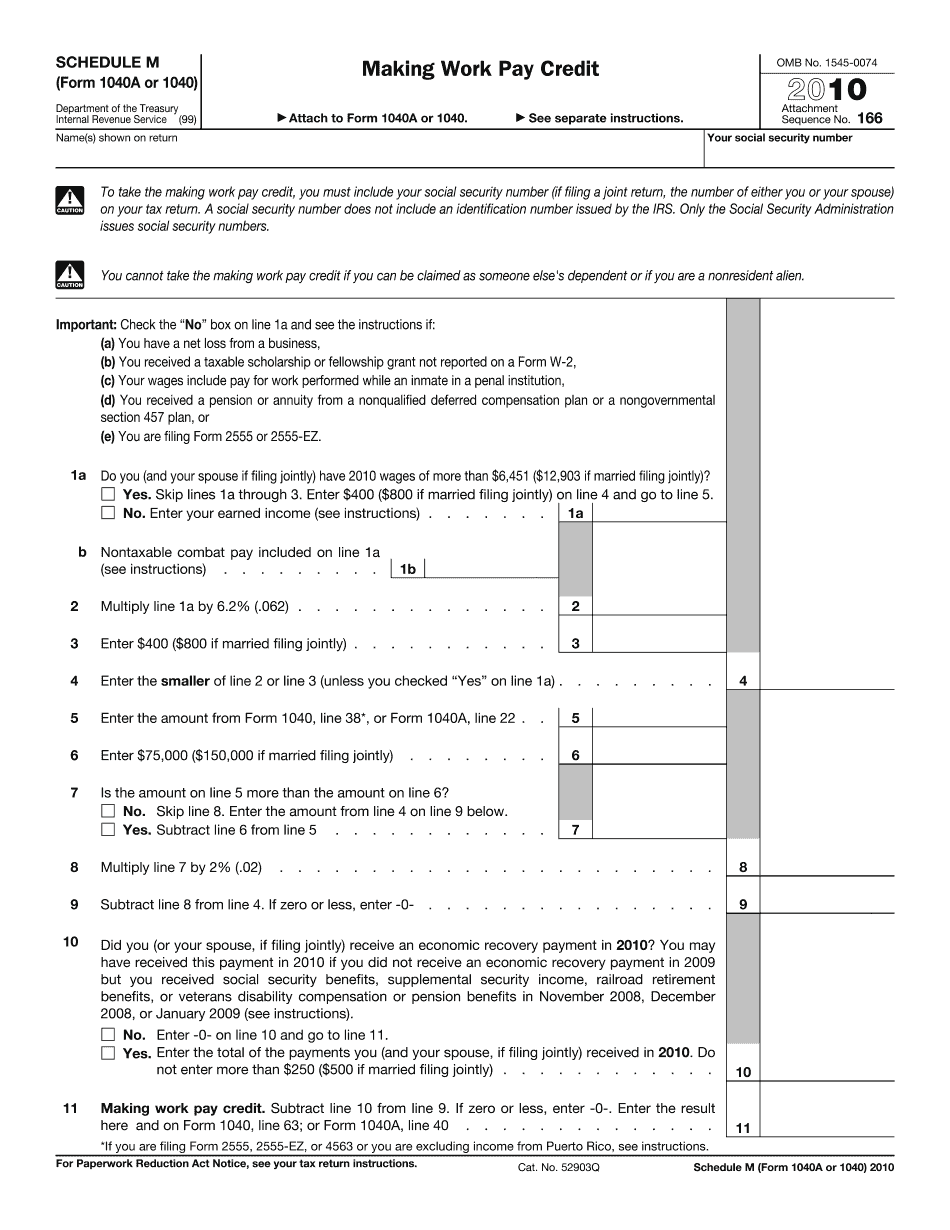

Award-winning PDF software

What is schedule m-3 Form: What You Should Know

The most important section details assets and other items that could be used to satisfy the 10 million thresholds. The “Account balance” and “Accounts receivable” tables must show “Cash of the partnership” if the partner reports cash (in the partnership funds) or another form of income or loss, whether the money is earned by the partner and whether the capitalized interest is reported. In this case, I would assume that your partners don't make money from the capitalized interest and thus, you don't need to show any figures here. Also, the amounts reported on the other tables may also be reported on one or more tables within the Summary table. These can all be found in the “Summary” section of the Schedule M-3. Please see the complete copy posted, which is also posted here (PDF). Form 1065-Nonresident Schedule M-3 is now for both non-resident and resident partners. They are considered to be different partners but are identical in the form. The non-resident partner should use the Schedule M-3 if the total assets are 10,000,000 or more and the partnership is a qualified electing partnership. The resident partner should use the Schedule M-3 if the partner and the partnership have 2 million or more in total assets and the partnership is not qualified electing. Here you can find both schedules. 1065/-5065 The Schedule M-3 for the first quarter of the partnership's tax year must be filed for non-resident partners if that partnership is qualified electing. The Schedule M-3 for the first quarter of the partnership's tax year cannot be filed if the partnership is not qualified electing. If 1065/ was used for 2017, you will not have to amend the partnership return for 2018. See: This Guide: 1065/-5065 Schedule M-3 for the first quarter of a Partnership's Tax Year. Schedule M-3 (Form 1065) (Rev. December 2021) — IRS The Schedule M-3 is being filed because (check all that apply): A amount of the partnership's total assets at the end of the tax year is equal to 10 million or more, or the partnership has a total tax liability in excess of 10,000,000. The amount of interest earned from certain partnerships.

Online solutions help you to manage your record administration along with raise the efficiency of the workflows. Stick to the fast guide to do Form 1040 - Schedule M, steer clear of blunders along with furnish it in a timely manner:

How to complete any Form 1040 - Schedule M online: - On the site with all the document, click on Begin immediately along with complete for the editor.

- Use your indications to submit established track record areas.

- Add your own info and speak to data.

- Make sure that you enter correct details and numbers throughout suitable areas.

- Very carefully confirm the content of the form as well as grammar along with punctuational.

- Navigate to Support area when you have questions or perhaps handle our assistance team.

- Place an electronic digital unique in your Form 1040 - Schedule M by using Sign Device.

- After the form is fully gone, media Completed.

- Deliver the particular prepared document by way of electronic mail or facsimile, art print it out or perhaps reduce the gadget.

PDF editor permits you to help make changes to your Form 1040 - Schedule M from the internet connected gadget, personalize it based on your requirements, indicator this in electronic format and also disperse differently.